Many people strive their entire lives to buy a house, but financial or personal reasons often get in the way. Taking out a bank loan to purchase a home is not uncommon, but what are the conditions and procedures? Let’s find out together.

1 Conditions for Installment Home Purchase Loan

To apply for a bank loan to buy a house in installments, you must meet the following requirements:

For the Borrower

- Must be a Vietnamese citizen or have a spouse who is a foreigner, aged 22-70, and have full legal and civil act capacity.

- Hold a household registration book/temporary residence book/temporary residence certificate as prescribed by the State.

- Provide personal documents: identity card/identity card, marriage certificate if married, or a certificate of single status from the local authority if single.

- Most importantly, the borrower must prove a stable income and the ability to repay the loan on time.

The prerequisite is that you must have Vietnamese citizenship

The prerequisite is that you must have Vietnamese citizenship

For the Borrower’s Income Level

Income from Basic Salary:

- Employment contract (still valid) or work assignment decision.

- Bank statements (original) of the salary account for the last 3-6 months or more, depending on the bank’s regulations.

The borrower’s income level must be supported by documents

The borrower’s income level must be supported by documents

Income Other Than Basic Salary:

- For income from rentals (house, car, etc.), you must provide documents proving ownership, such as a rental contract or receipts for the last three periods, legal documents of the rented property, and photos of the property.

- For business income: Business registration, financial statements, tax reports (last 3 years), income and expense records, bank statements, etc.

2 Procedures for Home Purchase Loan:

Step 1: Prepare the Necessary Documents

The required documents include:

- Loan application form (provided by the bank)

- Valid ID card/identity card

- Permanent residence book/temporary residence book/temporary residence certificate/temporary residence confirmation

- Marriage certificate

- Certificate of ownership of the house to be purchased and the purchase contract (copy)

- Proof of income: Employment contract, salary statements, or salary confirmation, payroll with the company’s seal.

- If the income source is from business activities, the customer must provide a business registration certificate, financial statements, and business reports for the last 6 months.

Step 2: Appraisal and Asset Evaluation

Based on the customer’s information and loan application, the bank will conduct an appraisal process, including checking the customer’s credit history, making phone calls, appraising the place of residence and work/business, and evaluating the collateral, which is the house being purchased.

Once the application meets the loan requirements, the bank will approve the loan

Once the application meets the loan requirements, the bank will approve the loan

Step 3: Make a Lending Decision and Disburse the Loan

If the application meets the loan requirements, the bank will send the customer a loan approval notice and proceed with the necessary procedures for disbursement.

Step 4: Monitor and Liquidate the Contract

After the purchase contract is notarized, the customer provides the contract to the bank, which then disburses the requested loan amount and transfers the funds to the seller’s account.

The process of obtaining a bank loan to buy a house usually takes about 2-3 days to a few weeks, depending on the customer’s application.

3 Methods of Home Purchase Loan:

Currently, banks offer various packages and flexible loan forms, allowing borrowers to take out a loan for up to 70-80% of the property’s value with a repayment period of up to 25 years, depending on the bank’s policies and promotions. Generally, there are two types of home purchase loans:

There are currently two types of loans: secured and unsecured

There are currently two types of loans: secured and unsecured

- Secured Loan: This type of loan uses your most valuable asset as collateral, which can be the house you are buying or another property. The advantage is that you can borrow a larger amount and have a longer repayment period of up to 35 years.

- Unsecured Loan: This option is more convenient as it does not require collateral and is based on the bank’s trust in the borrower. However, the repayment period is shorter, and the interest rate is higher.

4 Common Mistakes When Taking Out a Home Purchase Loan

Determining an Unsuitable Loan Amount

Although you can borrow up to 80% of the property’s value, it will put you under significant pressure due to the high-interest burden. Therefore, it is best to borrow around 30-40% of the property’s value, and allocate only 28% of your total income to repay the loan each month.

Choosing an Inappropriate Repayment Period

Similar to determining the loan amount, choosing a repayment period of about 25 years may reduce your financial burden, but it will create psychological pressure as you will be in debt for almost 25 years.

The loan amount, repayment period, and interest rate regulations are crucial factors to consider.

The loan amount, repayment period, and interest rate regulations are crucial factors to consider.

Not Understanding the Interest Rate Regulations

In addition to the above, it is essential to be aware of the interest rate regulations and any penalties for late payments or early full repayment of the loan. Also, note that you will receive a promotional interest rate for the first 1-2 years of the loan. Carefully consider all these factors before taking out a home purchase loan.

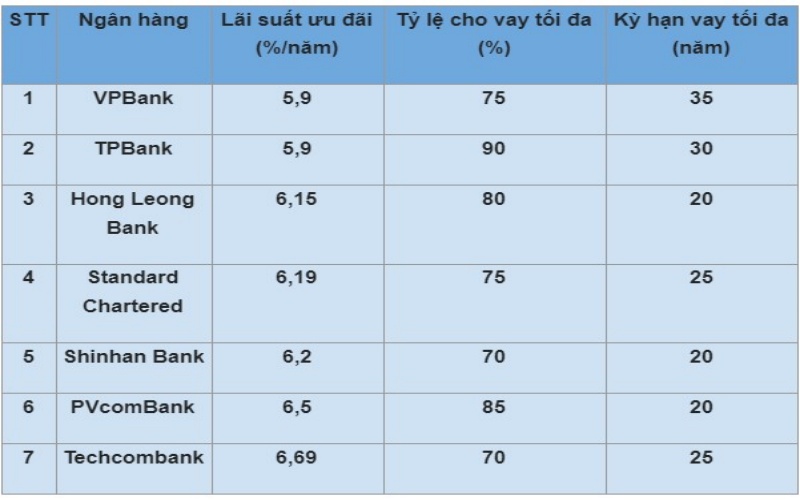

Reference: Interest rates of some banks (as of 5/2021)

The above information outlines the conditions and procedures for obtaining a bank loan to purchase a house. Hopefully, this will help those in need of a loan to navigate the process successfully.

Detailed instructions on how to check if a Viettel sim card is eligible for a loan in 2024

Do you know how to check for a Viettel sim loan? Currently, borrowing money through Viettel sims is a hot trend that many people are choosing due to its fast process and favorable interest rates. However, not every sim is eligible for this. Let’s find out more about this issue in the following article!

The Ultimate Guide to Agribank’s Hassle-Free Consumer Lending Process

If you’re looking to explore Agribank’s consumer lending procedures, then look no further!

The Ultimate Guide to Vietcombank Loan Procedures

“Securing a loan has become an increasingly common practice, and today we will guide you through the detailed step-by-step process of borrowing from Vietcombank. We’ll ensure you have all the information you need for a smooth and successful borrowing experience.”

{kind=link}