If you’re looking to import goods from overseas, you’ll need to go through customs procedures, but you may not know what that entails or what processes are involved. So, follow this article to learn everything you need to know about customs procedures!

1 What are Customs Procedures?

Customs procedures are mandatory processes that must be completed in over 200 countries and territories when importing/bringing goods and means of transport into a country and exporting/taking them out.

Customs procedures are carried out to provide a basis for tax calculations and to facilitate the management of imported/exported goods. This term refers to products, goods, or means of transport and is not applicable to people.

Customs procedures are mandatory in over 200 countries

Customs procedures are mandatory in over 200 countries

2 Detailed Import Customs Procedures

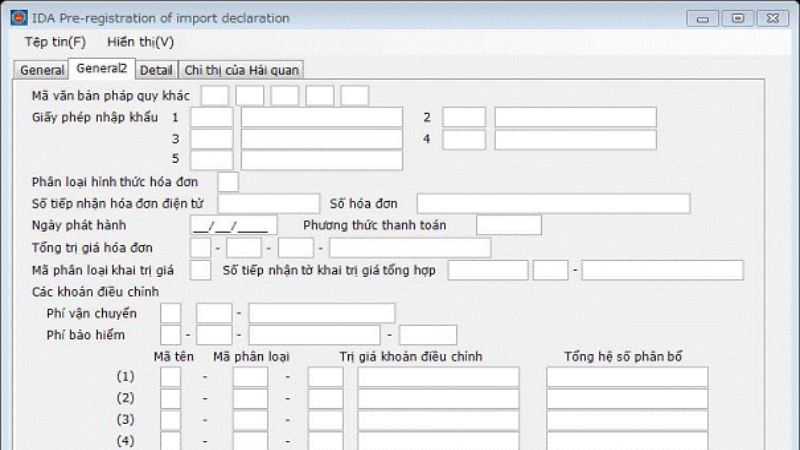

Import Information Declaration (IDA)

– The customs declarant will declare import information using the IDA function before registering the import declaration. After completing the 133 criteria on the IDA screen, the declarant must send it to the VNACCS system. The system will then assign a number and export relevant criteria related to tax rates, codes, etc., and provide feedback to the declarant on the import declaration registration screen (IDC).

– When the system assigns a number, the import information declaration (IDA) is stored in the VNACCS system.

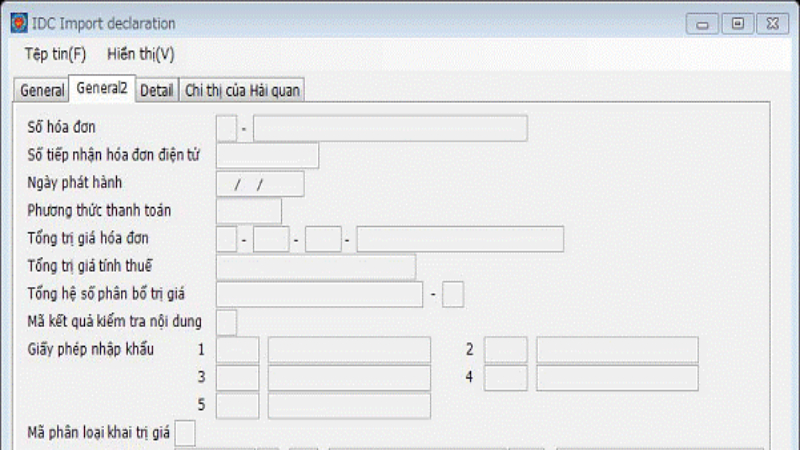

Import Declaration (IDC)

Import Declaration (IDC)

Import Declaration Registration (IDC)

After receiving the import declaration registration information on the screen, the customs declarant should review all the declared information and the information exported and calculated by the system.

+ If all information is correct and there are no errors, send it to the system to register the declaration.

+ If the declared information is incorrect, the declarant needs to make changes using the IDB function to recall the IDA screen and edit the information, following the instructions above. You can correct the declared information registered in the system countless times as there is no limit to the number of corrections.

Import Declaration (IDC)

Import Declaration (IDC)

Check the Conditions for Declaration Registration

After the customs declarant confirms the import declaration registration (IDC), the system will check the list of enterprises. If the enterprise is in a state of bankruptcy, dissolution, or has overdue debts of more than 90 days, the declaration will not be registered, and the system will notify the declarant.

Channel Allocation, Inspection, and Clearance

After the declaration is registered, the system will automatically allocate it into one of three channels: Green, Yellow, or Red.

Green channel declarations that have been cleared will be updated by the VNACCS system and transferred to the VCIS system at the end of the day

Green channel declarations that have been cleared will be updated by the VNACCS system and transferred to the VCIS system at the end of the day

For Green Channel Declarations:

– Case where the tax amount payable is 0:

The system will grant clearance (expected time: 3 seconds) and issue the “Decision on Import Goods Clearance” to the declarant.

– Case where the tax amount payable is not 0:

+ If the tax payment by limit or guarantee (common or separate) has been declared, the system will check the relevant criteria for the limit and guarantee.

If the limit or guarantee amount is greater than or equal to the tax amount payable, the system will display the “Tax Collection Note” and the “Decision on Import Goods Clearance” on the screen. However, if the limit or guarantee amount is less than the tax amount payable, the system will report an error.

+ If the tax payment immediately (by transfer or cash at the customs office) has been declared:

The system will display the “Tax Collection Note” on the screen and issue the “Decision on Import Goods Clearance” after the declarant pays the taxes, fees, and charges, and it is recorded by the VNACCS system.

Note: All green channel declarations that have been cleared will be compiled by the VNACCS system and transferred to the VCIS system at the end of the day.

For Yellow and Red Channel Declarations

Data from yellow and red channel declarations will be transferred from the VNACCS system to the VCIS system.

a. Customs Authority

* Perform declaration checks and processing on the VCIS system screen:

– Leader: Note the instructions from the assigned official regarding the declaration check and processing in the corresponding box on the “Declaration Check Screen.”

– Assigned Official: Note the suggestions, the contents requiring the leader’s opinion, and the results of the declaration check and processing in the corresponding box on the “Declaration Check Screen.”

– The system will not allow the CEA function to be performed if the leader and the assigned official do not acknowledge the contents on the screen.

* Use the CKO function:

– Notify the customs declarant about the location, form, and level of physical inspection of goods (for goods in the red channel).

– To switch channels from red to yellow or vice versa. This switch depends on the regulations of the relevant business process.

* Use the CEA function:

– For the yellow channel, enter “Completed File Check.”

– For the red channel, enter “Completed File and Physical Inspection of Goods.”

* Use the IDA01 function to enter instructions/requests for procedures, amendments to the declaration, tax imposition, and send them to the customs declarant for implementation.

b. Customs Declarant

At this stage, the customs declarant needs to do the following:

– Receive system feedback on channel allocation results, location, form, and level of physical inspection of goods.

– Submit paper documents for detailed file inspection by the customs authority and prepare conditions for the physical inspection of goods.

– Fulfill all obligations regarding taxes, fees, and charges (if any).

c. System

For yellow and red channels, the system is responsible for:

– Issuing the “Customs Declaration” to the declarant. The declaration clearly states the channel allocation results in the “Inspection Classification Code” criterion.

– Issuing a “Notification of Physical Inspection of Goods” for goods allocated to the red channel or when the customs authority uses the CKO function to switch channels.

– Immediately after the customs authority completes the CEA function, the system will automatically perform the following tasks:

+ If the tax amount payable is 0:

The system will grant clearance and issue the “Decision on Import Goods Clearance” to the declarant.

+ If the tax amount payable is not 0:

If the tax payment by limit or guarantee (common or separate) has been declared, the system will check the relevant criteria for the limit and guarantee. If the limit or guarantee amount is greater than or equal to the tax amount payable, the system will display the “Tax Collection Note” and the “Decision on Import Goods Clearance” on the screen. However, if the limit or guarantee amount is less than the tax amount payable, the system will report an error.

If the tax payment immediately (by transfer or cash at the customs office) has been declared: The system will display the “Tax Collection Note” on the screen and issue the “Decision on Import Goods Clearance” after the declarant pays the taxes, fees, and charges, and it is recorded by the VNACCS system.

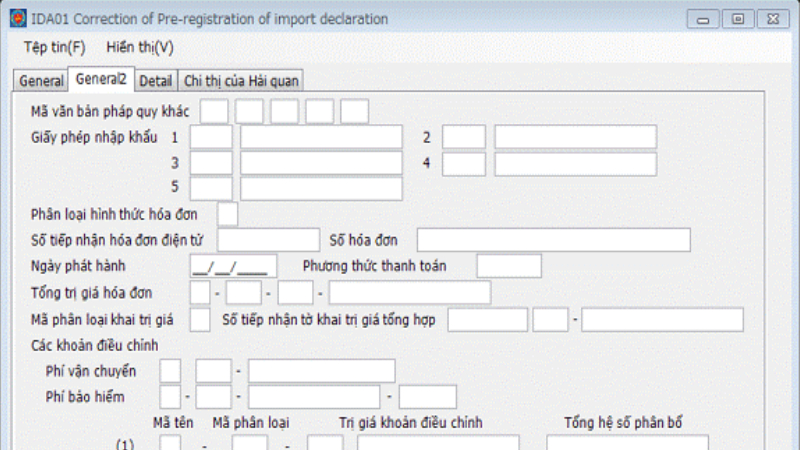

Amendment Declaration during Clearance

– After registering the declaration and before clearing the goods, the system allows the declarant to make amendments. To do this, the customs declarant must use the IDD function to call up the amendment declaration information screen.

+ If this is the first amendment declaration, the screen will display all the information from the import declaration (IDA).

+ If it is the second time or more, the screen will display the amended import declaration information updated in IDA01.

– Once the declaration has been completed in IDA01, the customs declarant needs to send it to the VNACCS system to obtain a declaration number and receive feedback on the amendment declaration information on the IDE screen. When the declarant clicks “Send” on the IDE screen, the amendment declaration registration is completed.

IDA01 Declaration

IDA01 Declaration

– The amendment declaration number is the last character of the declaration number, and the declarant can make up to 9 amendment declarations, corresponding to the last character of the declaration number from 1 to 9. If no amendments are made during clearance, the last character of the declaration number will be 0.

– When the customs declarant makes an amendment declaration, the declaration can only be allocated to the yellow or red channel (not the green channel).

– The criteria on the amendment declaration information screen (IDA01) will be similar to the criteria on the import information declaration screen (IDA). However, some criteria (as specified in the IDA01 guide) cannot be entered in IDA01 as they cannot be amended or are not subject to amendment.

Points to Note

Each declaration can have a maximum of 50 items

If a shipment has more than 50 items, the customs declarant will need to make declarations on multiple forms, and the forms for the same shipment will be linked based on the branch number of the declaration.

Taxable Value

– Declare the taxable value: Combine the criteria of the taxable value declaration according to method 1 with the import declaration. For other methods, only combine some result criteria with the import declaration, and the specific calculations for the taxable value according to each method must be made on a separate taxable value declaration.

– Automatic calculation: For shipments eligible for the transaction value method, the customs declarant declares the Total Invoice Value, the total allocation factor, the invoice value of each item, adjustments, and the allocation factor for adjustments. Based on this, the system will automatically allocate the adjustments and automatically calculate the taxable value for each item.

– No automatic calculation: For shipments eligible for the transaction value method but with more than 5 adjustments other than I and F, or if the allocation of adjustments is not proportional to the value, the system will not automatically allocate or calculate the taxable value. For these cases, the customs declarant declares and calculates the taxable value for each item on a separate taxable value declaration, and then enters the result in the “taxable value” box of each item.

Each declaration can have a maximum of 50 items, and the taxable value needs to be noted

Each declaration can have a maximum of 50 items, and the taxable value needs to be noted

Tax Rate

When the customs declarant performs the import information declaration function (IDA), the system will apply the exchange rate on the date of this function to automatically calculate the tax.

– The system will maintain the tax rate if the customs declarant performs the import information declaration function (IDA) and registers the import declaration (IDC) on the same day or on two days with the same exchange rate.

– The system will report an error if the customs declarant performs the import declaration registration function (IDC) (considered the time when the declarant clicks “Send” on the IDC screen) on a day with a different exchange rate than the day of the import information declaration (IDA). In this case, the declarant needs to use the IDB function to call up the IDA and declare it again – essentially, just call up the IDA and send it, and the system will automatically update the exchange rate according to the IDC registration date.

Tax Rate

– When the customs declarant performs the import information declaration function (IDA), the system will use the tax rate on the expected IDC declaration date to automatically fill in the tax rate box.

– If the tax rate on the expected IDC declaration date is different from the tax rate on the actual IDC declaration date, the system will report an error when the customs declarant performs the import declaration registration function (IDC). Therefore, the declarant needs to use the IDB function to call up the IDA and declare it again – essentially, just call up the IDA and send it, and the system will automatically update the tax rate according to the IDC declaration date.

– If the customs declarant manually enters the tax rate, the system will display “M” next to the tax rate box.

Simple, Accurate, and Convenient Guide to Customs Declaration Lookup

Looking up customs declarations is no longer as complicated as it used to be. The following article will guide you on how to easily, quickly, and accurately search for customs declarations. Follow the instructions below to save time for your business.

Customs Clearance Simplified: Unraveling the Intricacies of Import and Export Procedures

Join us as we delve into the fascinating world of export customs procedures and uncover any changes in the basic process. It’s time to explore and demystify the intricacies of international trade, ensuring a smooth journey for your goods across borders.

“A Comprehensive Guide to Importing Goods from China to Vietnam”

Introducing the ultimate guide to navigating the complex world of importing goods from China to Vietnam. Unravel the mysteries of cross-border trade with our comprehensive step-by-step process, empowering you to expand your business horizons with ease and efficiency. Discover the secrets to seamless importing, ensuring your venture is a resounding success.

“A Comprehensive Guide to Vehicle Tax Procedures: Understanding the Process for New and Used Car Registrations in 2021”

Submitting the registration fee for your car, whether it’s brand new or a second-hand purchase, is an essential step in the process of car ownership. Today, we will guide you through the ins and outs of this procedure, ensuring you’re well-informed about the car registration fee process for 2021 and beyond.

{kind=link}