Liquidation of Fixed Assets: A Comprehensive Guide to the Process

1 Understanding Fixed Assets

An example of fixed assets

An example of fixed assets

According to Article 2 of Circular No. 45/2013/TT-BTC, there are two types of fixed assets based on legal grounds:

- Tangible fixed assets: These are main means of labor that have a physical form and meet the criteria of tangible fixed assets. They are used in multiple business cycles while retaining their original physical form, such as buildings, structures, machinery, equipment, and vehicles.

- Intangible assets: These are assets that do not have a physical form but represent a value that has been invested. They meet the criteria of intangible fixed assets and are used in multiple business cycles. Examples include certain land-related costs, issuance rights, patents, and copyrights.

As per Article 35, Circular No. 200, fixed assets are defined as tangible means of labor that simultaneously meet the following conditions as stipulated by law:

-

The use of the asset will definitely bring economic benefits in the future.

-

The asset has a useful life of one year or more.

-

The original cost of the asset must be accurately determined according to the law and must be valued at VND 30,000,000 or more.

Additionally, a related concept is independent tangible fixed assets. In a system comprising multiple individual assets that are interconnected, each component may have a different useful life from the others. If one of these components is missing, the system can still perform its main function. Depending on the requirements for use and management, each component must be managed separately and meet all three conditions mentioned above as stipulated by law to be considered an independent tangible fixed asset.

2 When to Liquidate Fixed Assets in a Business

Decision to liquidate fixed assets when they become obsolete

Decision to liquidate fixed assets when they become obsolete

The following are the situations when a business can liquidate fixed assets:

-

The fixed asset is damaged and cannot be used anymore.

-

The fixed asset has become technologically and technically obsolete and no longer meets the production and business requirements of the enterprise.

-

When the enterprise is sold, dissolved, or merged.

3 Liquidation Process for Fixed Assets

When there is a need to liquidate fixed assets, the enterprise must make a decision to liquidate and establish a fixed asset liquidation council. According to regulations, the liquidation council is responsible for organizing the liquidation of fixed assets according to the prescribed financial management procedures and establishing a fixed asset liquidation report following these steps:

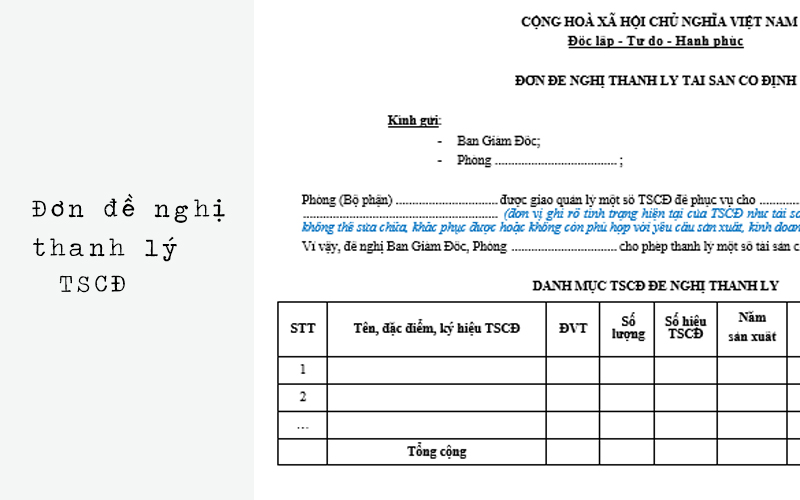

Step 1 Establish a Request for Liquidation of Fixed Assets

Request for liquidation of fixed assets

Request for liquidation of fixed assets

The request for liquidation of fixed assets is regulated by Form No. 2-TSCD (according to Decision 48/2006/QD-BTC). The request must be submitted to the company’s leadership for approval based on the results of the fixed asset inventory and the process of monitoring and using fixed assets in the enterprise, department, or unit where the fixed asset to be liquidated is located. Note that the request must clearly list the fixed assets to be liquidated.

Step 2 Decision to Liquidate Fixed Assets

Decision to liquidate fixed assets

Decision to liquidate fixed assets

The representative of the enterprise will be the person who makes the decision to liquidate the fixed assets.

Step 3 Establishment of the Fixed Asset Liquidation Council

Establishment of the Fixed Asset Liquidation Council

Establishment of the Fixed Asset Liquidation Council

The Fixed Asset Liquidation Council is responsible for inspecting, evaluating, and organizing the liquidation of fixed assets in accordance with the prescribed financial management procedures and establishing a liquidation report for fixed assets. Accordingly, the fixed asset liquidation council comprises:

-

Head of the unit: Chairman of the Council.

-

Chief Accountant: In charge of fixed asset accounting.

-

Head or Deputy Head of the Infrastructure Department: Officer in charge of fixed assets.

-

Representative of the unit directly managing the fixed assets to be liquidated.

-

Officer with knowledge and understanding of the technical characteristics and functions of the fixed assets to be liquidated.

-

May include representatives of unions and people’s inspectors.

Step 4 Liquidation of Fixed Assets

Liquidation of fixed assets

Liquidation of fixed assets

The Fixed Asset Liquidation Council presents to the head of the enterprise the proposed form of fixed asset disposal, either destruction or sale, depending on the characteristics and conditions of the fixed assets.

Step 5 Establishment of the Fixed Asset Liquidation Report

Fixed Asset Liquidation Report

Fixed Asset Liquidation Report

After liquidating the fixed assets, the Fixed Asset Liquidation Council will establish a fixed asset liquidation report. According to regulations, for fixed assets that are large-scale infrastructure works with values funded by the state budget and managed, operated, and used by economic organizations, the liquidation must be agreed upon in writing by the representative agency of the state owner and accounted for in the reduction of the enterprise’s business capital.

The above is the process of liquidating fixed assets of an enterprise that you should know. Hopefully, the information provided has helped you understand fixed assets and the process of liquidating fixed assets. Please visit us for more interesting information!

{kind=link}