According to Decree No. 119/2018/ND-CP, the registration of electronic invoices is a mandatory legal procedure for businesses established after November 1, 2018. Today, we will guide you through the detailed process and procedures for registering electronic invoices.

1 What is an Electronic Invoice?

According to Circular No. 32/2011/TT-BTC dated March 14, 2011, of the Ministry of Finance:

An electronic invoice is a collection of electronic data messages about the sale of goods and the provision of services, which are created, established, sent, received, stored, and managed by electronic means. Electronic invoices must meet the content requirements specified in Article 6 of this Circular.

Electronic invoices are created, issued, processed, and stored on the computer systems of organizations that have been assigned tax codes when selling goods and services, in accordance with the law on electronic transactions.

An electronic invoice is a collection of electronic data messages about the sale of goods and services, stored and managed by electronic means.

An electronic invoice is a collection of electronic data messages about the sale of goods and services, stored and managed by electronic means.

Electronic invoices include the following types: export invoices; value-added tax invoices; sales invoices; other invoices including: stamps, tickets, cards, insurance premium receipts…; air transport cargo receipts, international transport cargo receipts, bank service charge receipts… The format and content of these invoices are established according to international practices and relevant legal provisions.

Electronic invoices ensure the following principles: the invoice number must be consecutive and in chronological order, and each invoice number must be used only once.

2 Registration Procedure for Electronic Invoices with a Tax Code

Applicable Entities

The entities eligible to register for electronic invoices with a tax code include both enterprises and households.

The entities eligible to register for electronic invoices with a tax code include both enterprises and households.

The procedure for registering to use electronic invoices with a tax code applies to the following entities:

Organizations and Enterprises:

- Use electronic invoices with a tax code when selling goods and providing services.

- Belong to the high-tax-risk category.

Households and Individuals Engaged in Business, whether or not they are required to maintain accounting books, and regularly employ 10 or more employees:

- For the fields of agriculture, forestry, fisheries, industry, and construction: Applicable to enterprises with annual revenue of VND 3 billion or more in the previous year.

- For the fields of trade and services: Applicable to enterprises with annual revenue of VND 10 billion or more in the previous year.

How to Register for Electronic Invoices with a Tax Code?

To register to use electronic invoices with a tax code, follow the steps below:

Portal of the General Department of Taxation.

Portal of the General Department of Taxation.

Access the portal of the General Department of Taxation at the address: http://www.gdt.gov.vn/wps/portal.

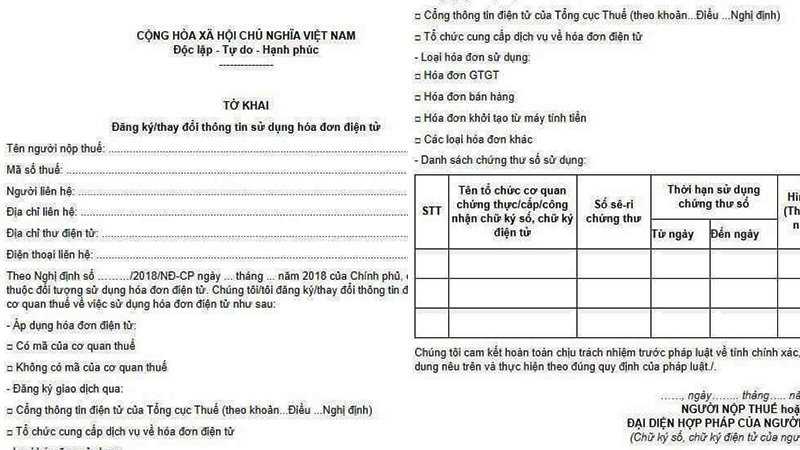

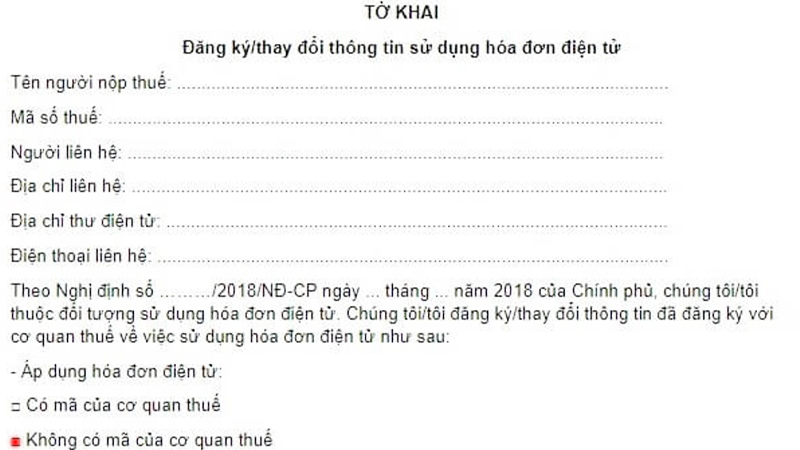

Form No. 1, Appendix to Decree 119/2018.

Form No. 1, Appendix to Decree 119/2018.

Fill in the registration information according to Form No. 01, Appendix to Decree 119/2018. Remember to select the box “With a tax code” in the “Apply for Electronic Invoices” section.

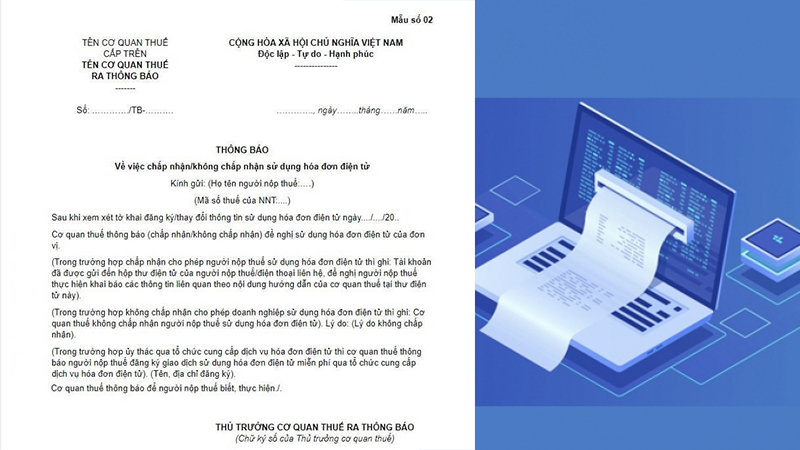

Form No. 2, Appendix to Decree 119.

Form No. 2, Appendix to Decree 119.

Wait for the tax authority to send a notification according to Form No. 2, Appendix to Decree 119. Within 1 day from the date of receipt of the electronic invoice registration, you will receive a notification from the tax authority.

Note:

- When starting to use electronic invoices, you must cancel all unused paper invoices according to the regulations.

- If you need to change the registered information, you can modify it based on Form No. 1 and resubmit it to the tax authority.

Cases of Discontinuing the Issuance of Electronic Invoice Codes

Some cases where the use of electronic invoices is discontinued.

Some cases where the use of electronic invoices is discontinued.

The following are the cases where the issuance of electronic invoice codes is discontinued:

- The entity’s tax code has expired.

- The entity is found by the tax authority to be inactive at the registered address.

- The entity has notified the competent state management agency of its temporary suspension of business.

- The entity has received a notification from the tax authority about the discontinuation of electronic invoices to enforce tax debt collection.

- The entity uses electronic invoices with a tax code to sell smuggled, prohibited, counterfeit, or intellectual property-infringing goods, and this is detected and reported to the tax authority.

- The entity issues electronic invoices with a tax code to fake the sale of goods or services to defraud individuals or organizations, and this is detected and reported to the tax authority.

- The enterprise does not meet the business conditions, and its business registration is temporarily suspended by the business registration authority or a competent state agency.

3 Registration Procedure for Electronic Invoices without a Tax Code

Applicable Entities

Entities using electronic invoices without a tax code must comply with Clause 1, Article 20 of Decree 119, and the organizations and enterprises specified in Clause 2, Article 12.

Entities using electronic invoices without a tax code must comply with Clause 1, Article 20 of Decree 119, and the organizations and enterprises specified in Clause 2, Article 12.

According to Clause 1, Article 20 of Decree 119, the organizations and enterprises specified in Clause 2, Article 12 that can register to use electronic invoices without a tax code include:

- Enterprises operating in the following fields: petroleum, electricity, postal and telecommunications services, air, rail, road, and water transport, clean water supply, finance and credit, healthcare, insurance, e-commerce, supermarkets, and trade.

- Enterprises and economic organizations that have or will conduct transactions with tax authorities by electronic means, build information technology infrastructure, have accounting software and electronic invoice issuance software that meet the requirements, and can ensure the transmission of electronic invoice data to both the buyer and the tax authority.

Registration Procedure for Invoices without a Tax Code

The procedure for registering to use invoices without a tax code includes the following steps:

Portal of the General Department of Taxation.

Portal of the General Department of Taxation.

Access the portal of the General Department of Taxation at the address: http://www.gdt.gov.vn/wps/portal.

Fill in the information according to Form No. 01, Appendix to Decree 119/2018.

Fill in the information according to Form No. 01, Appendix to Decree 119/2018.

Fill in the registration information according to Form No. 01, Appendix to Decree 119/2018, and select the box “Without a tax code” in the “Apply for Electronic Invoices” section.

Wait for the tax authority to send a notification according to Form No. 2, Appendix to Decree 119. Within 1 day from the date of receipt of the electronic invoice registration, you will receive a notification from the tax authority.

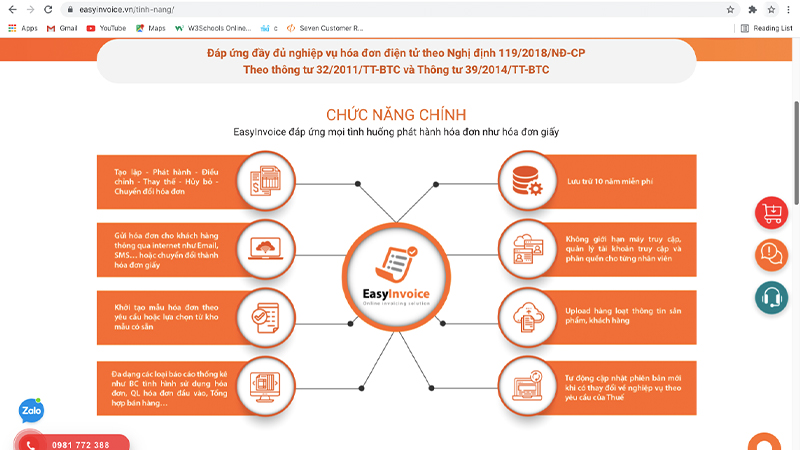

4 EasyInvoice – Simple and Convenient Electronic Invoice Registration Procedure

Procedure for Providing EasyInvoice Electronic Invoices to Customers

EasyInvoice website.

EasyInvoice website.

The following are the detailed steps of the procedure for providing EasyInvoice electronic invoices:

Take photos or scan the business license and ID card/CCC of the legal representative and send them to the support staff via Zalo or email.

Send the logo (if any) to EasyInvoice so that they can create an invoice template and send it to you for approval.

Choose a suitable package and proceed to sign an electronic contract.

Handover Procedure after Successful Registration

EasyInvoice provides you with all the functions according to Decree 119/2018.

EasyInvoice provides you with all the functions according to Decree 119/2018.

After completing the registration procedure, the EasyInvoice staff will proceed with the following handover:

- Provide an account to access the EasyInvoice electronic invoice system.

- Install the EasyInvoice electronic invoice system.

- Provide guidance on using the EasyInvoice electronic invoice system via team view, ultra view, hotline, etc.

Did you know: According to Clause 1 and Clause 3 Article 59 of Decree 123:

1. This Decree takes effect from July 1, 2022, and encourages agencies, organizations, and individuals who meet the conditions of information technology infrastructure to apply the provisions of this Decree on electronic invoices and vouchers before July 1, 2022.

3. Clause 2 and Clause 4 of Article 35 of Decree No. 119/2018/ND-CP dated September 12, 2018, of the Government, prescribing electronic invoices, shall be annulled as of November 1, 2020.

In addition, Clause 1, Article 60 also stipulates that enterprises and economic organizations are allowed to use paper invoices until June 30, 2022, for invoices that have been notified of issuance before October 19, 2020.

Thus, the use of electronic invoices is only mandatory from July 1, 2022, and the regulation on mandatory use from November 1, 2020, is annulled.

5 Notes on the Procedure for Registering Electronic Invoices

Notes on the procedure for registering electronic invoices.

Notes on the procedure for registering electronic invoices.

Case of Acceptance

In

What is EasyInvoice bill lookup? Is it accurate? Step by step guide on how to do it

You can easily check your EasyInvoice bills by using the downloadable software on your computer or by checking online on the website. If you are a partner business of EasyInvoice or a customer of these businesses, please follow the steps below for bill lookup.

{kind=link}